The study’s full report is available here.

The ongoing COVID-19 pandemic has raised countless questions about its impact on the artists and creatives, and, more specifically, on their audiences. How has the pandemic changed audiences’ desire to participate in cultural events? Have audiences found new ways in which to consume cultural activity, turning more towards online viewership at a time when physical gatherings are limited? Will we see new patterns of attendance emerge once the pandemic has subsided?

These are amongst the questions driving a study carried out by Arts Council Malta investigating the changing relationship between Public Cultural Organisations and audiences to cultural events in light of the ever-changing public health situation over the past months.

The study is composed of two strands:

The first telephone survey was carried out amongst 540 respondents throughout the months of November and December 2020, with a second wave of the survey was carried out amongst 504 respondents throughout January and February 2021. The third and final survey was carried out throughout July 2021. All survey samples were representative of the general population.

The findings of this study shed light on the ways in which the public’s views on cultural events have changed throughout the pandemic and its developments over the past months and will be used to provide Public Cultural Organisations with recommendations on how to further strengthen their ongoing audience engagement, and strategically explore new forms of growth.

Findings from 1st survey

This telephone survey was carried out amongst 540 respondents throughout the months of November and December 2020. The survey sample was representative of the general population.

During the initial lockdown period (March-May 2020), the most followed online events were theatre performances (9%) and concerts/music performances (9%), with a further 9% and 7% respectively expressing an interest in viewing online performances in these fields in the future. On the whole, respondents tended to follow online events fairly equally on local and international websites/platforms, although respondents between the ages of 25-34 and 55-64 indicated a slight preference towards viewing on local websites/platforms. Online viewership was generally highest for 35-44 age group, but interest in viewing cultural activity online in the future was highest amongst younger age groups (18-24 and 25-34).

Once the initial lockdown was eased in June 2020 and physical gatherings came back into being, physical attendance to cultural events remained negligible, with respondents showing little inclination to attend in-person events over the next six months. This was the case across all forms of cultural activity, with the many respondents expressing an intention to wait for a vaccine to be administered before returning to in-person events. 32% of all respondents cited “having a vaccine” as a key factor in enticing them to return to physical cultural activity. Other factors frequently mentioned included “enforcement of COVID-19 restrictions” (17%) and “restricted audience sizes” (8%).

These findings indicate that online participation is here to stay, regardless of the pandemic, with 53% of respondents expect their online participation to increase or stay the same in the future, even once the pandemic ends.

There are also indications that several respondents would be receptive to different payment models for online cultural activity. 12% are willing to give a donation upon viewing an online performance, 10% are willing to pay through a pay per view system, and 7% are willing to pay towards a yearly subscription model for online cultural events.

The study’s respondents were also aware of the need to financially support the local cultural sector – over a third of respondents (34%) agreed that they are willing to pay for events that were previously free, and 31% are willing to pay a higher-than-average ticket price for events (up to 10% higher). Furthermore, almost half the respondents (49%) are willing to give a one-time donation to cultural organisations, and a third (33%) are willing to contribute to a crowdfunding campaign to assist cultural organisations.

Findings from 2nd survey

The initial survey found that the most followed online events during lockdown period (March-May 2020) were theatre performances and concerts/music performances, with 9% of respondents stating that they followed either of these type of events through local or international online platforms. However, the second wave of data collection shows decreased rates of online participation during the same period, where the highest rate of participation was registered for concerts/music performances, with 4% of respondents watching either through local or international online channels. Similarly, lower levels of attendance to online events were recorded across all artistic disciplines.

On the other hand, respondents in the second wave of data collection expressed a slightly higher degree of interest in attending events in person in the near future, compared to the first survey, with 7% of respondents stating that they may visit a museum over the next 6 months and a further 7% that they may visit a historical site over the same period (up from 2% and 3% respectively). Nonetheless, the intention to attend events that involve a live audience (such as theatre, concerts/live music performances, or festivals) remained relatively low and in line with the first survey, with none of these types of events attracting more than 4% of respondents to attend over the next 6-month period.

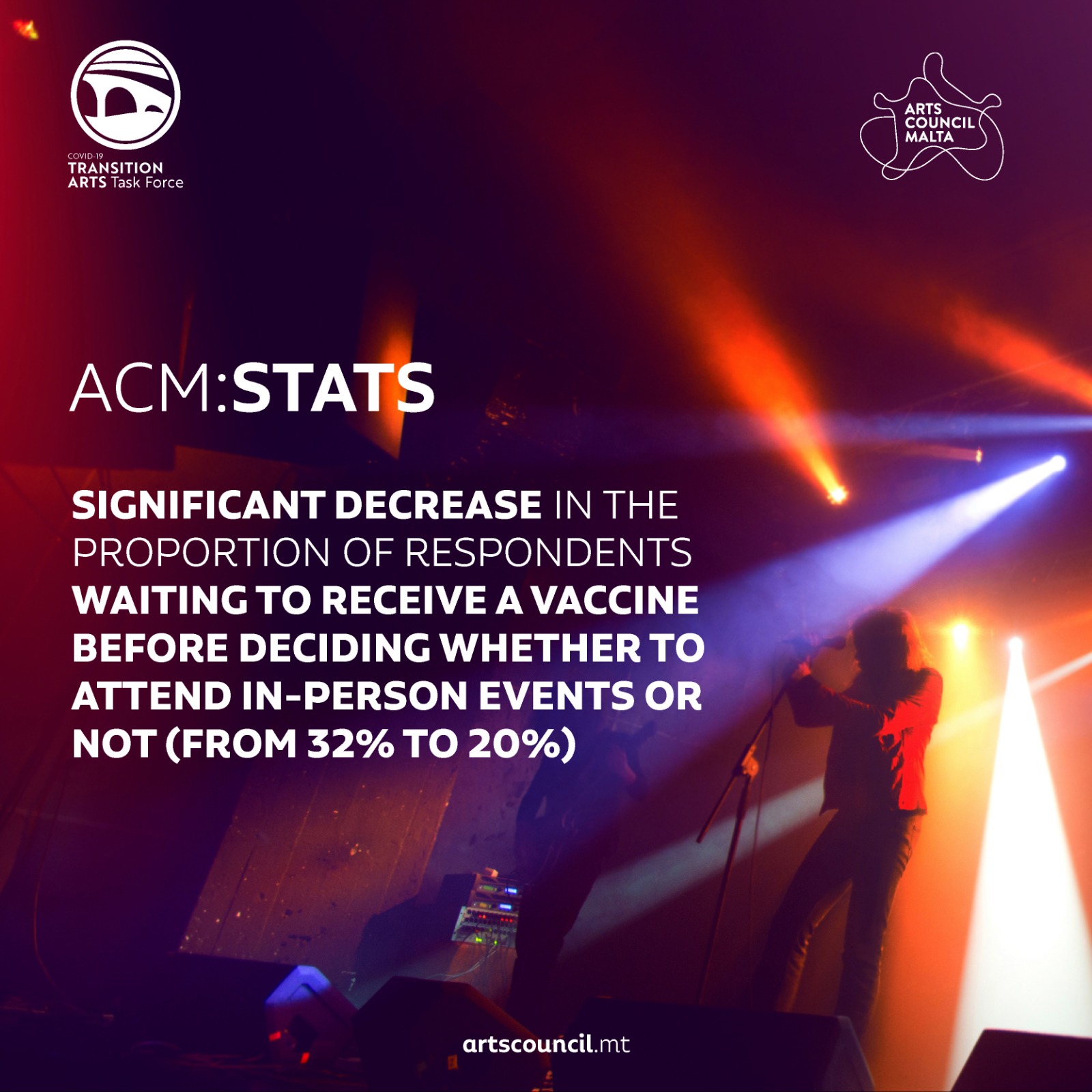

There was, however, a significant decrease in the proportion of respondents waiting to receive a vaccine before deciding whether to attend in-person events or not. Whereas the first survey found that 32% of respondents interested in live theatre were waiting to receive a vaccine before returning to in-person attendance, this decreased to 17% in the second survey. A similar pattern was seen amongst respondents interested in concerts/live music performance, with a decrease from 29% to 17%. Likewise, while “having a vaccine” was a key factor in returning to any type of live event for 32% of respondents in the first survey, this registered a decrease of 8 percentage points (32% to 24%) in the second survey.

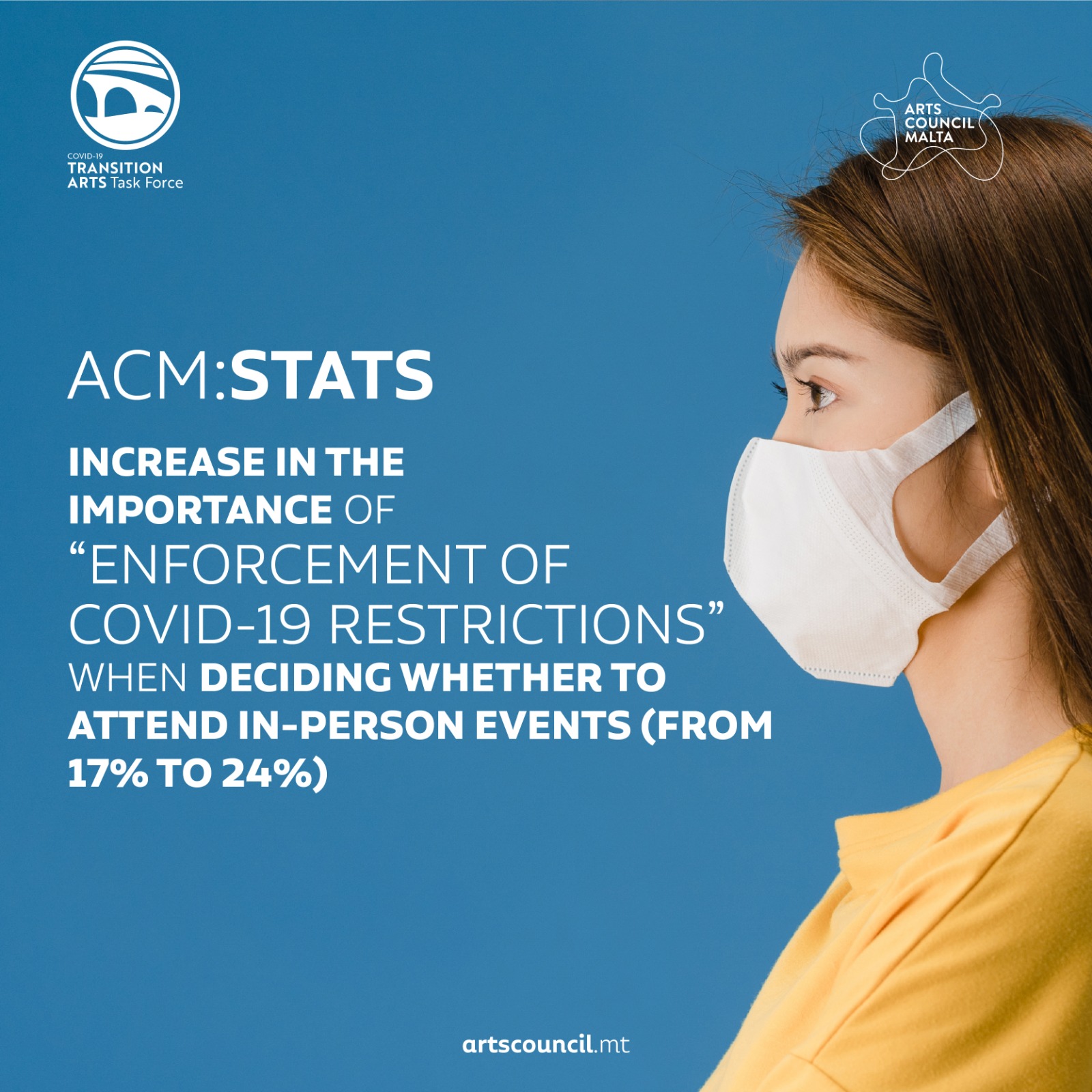

As time progresses, respondents seem to place a greater emphasis on the “enforcement of COVID-19 restrictions” (up 7 percentage points, from 17% to 24%) and outdoor performances (up 2 percentage points, from 6% to 8%). These findings are likely to be indicative of the broader public health situation across the country, with the national vaccine rollout having begun in the period between the two surveys being held.

On the whole, respondents to the second survey seemed to indicate a growing degree of weariness with online viewership of cultural events. 70% of respondents expect their online participation in cultural activity to decrease in the next 12 months regardless of whether the pandemic ends or not (up from 47% in the first survey), while only 1% of respondents believe that their online participation is set to increase.

The second survey also confirms the public’s willingness to financially support cultural activity, albeit at a lower level than the first survey. Compared to the initial survey, respondents are less willing to pay for online events, reflecting their general weariness with online activity. In fact, respondents are less inclined to give a donation (3%, down from 12%) or pay per view (3%, down from 10%) for online events, and they are also less likely to pay for yearly (3%, down from 7%) or monthly (2%, down from 6%) subscriptions for online events or activities. However, there are still relatively high levels of willingness to pay for in-person events. 30% of respondents indicated that they are willing to pay for events that were previously free (compared to 34% in the first survey), 21% would pay a higher than usual price to attend an event (31% in the previous survey), and 39% would consider giving a cultural organisation a one-time donation (49% in the previous survey). The findings also show an increase in willingness to attend more local cultural events (28%, up from 24%) or join a cultural organisation’s membership scheme to support local artists (16%, up from 13%).

There are also indications that several respondents would be receptive to different payment models for online cultural activity. 12% are willing to give a donation upon viewing an online performance, 10% are willing to pay through a pay per view system, and 7% are willing to pay towards a yearly subscription model for online cultural events.

Final findings

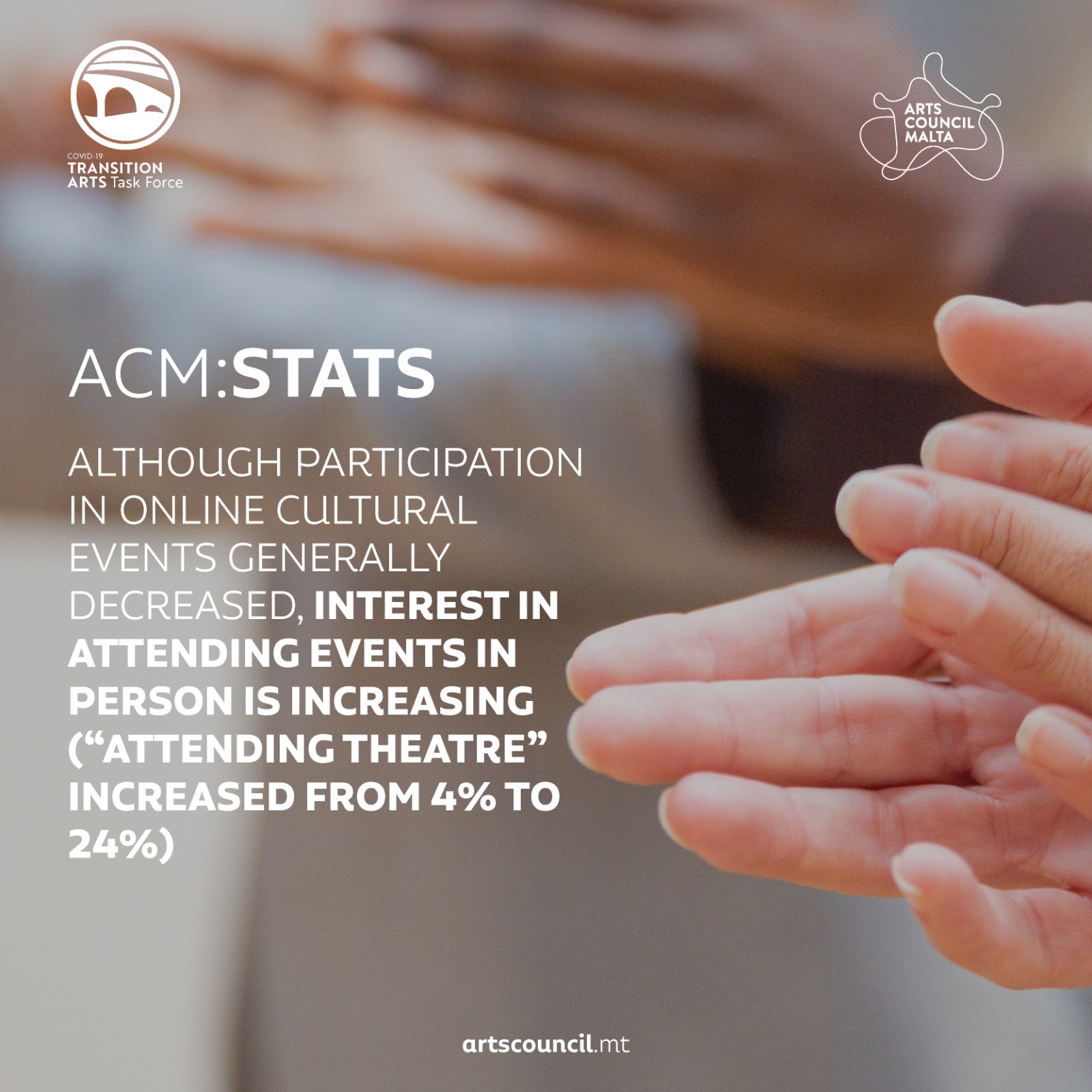

Overall, 73% of respondents attended one or more cultural event in the 12 months preceding the COVID-19 pandemic. Following the easing of lockdown restrictions, audiences have not yet returned to attending in-person events at the same frequency as they did prior to the pandemic. Nonetheless, interest in attending in-person cultural events is increasing over time, with interest in attending live theatre performances over the next six months growing from 4% in the first survey to 24% in the third.

During lockdown, the number of people that shifted to following cultural events online was relatively low, with the highest rates of participation registered for live concerts and theatre, both at 7%. The rate of online engagement generally decreased from one survey to the next and respondents indicated that they are likely to decrease their engagement with online cultural events in the future. In fact, the study found that 83% of respondents expect their online participation in cultural activity to decrease over the next 12 months, regardless of whether the pandemic ends or persists over this period.

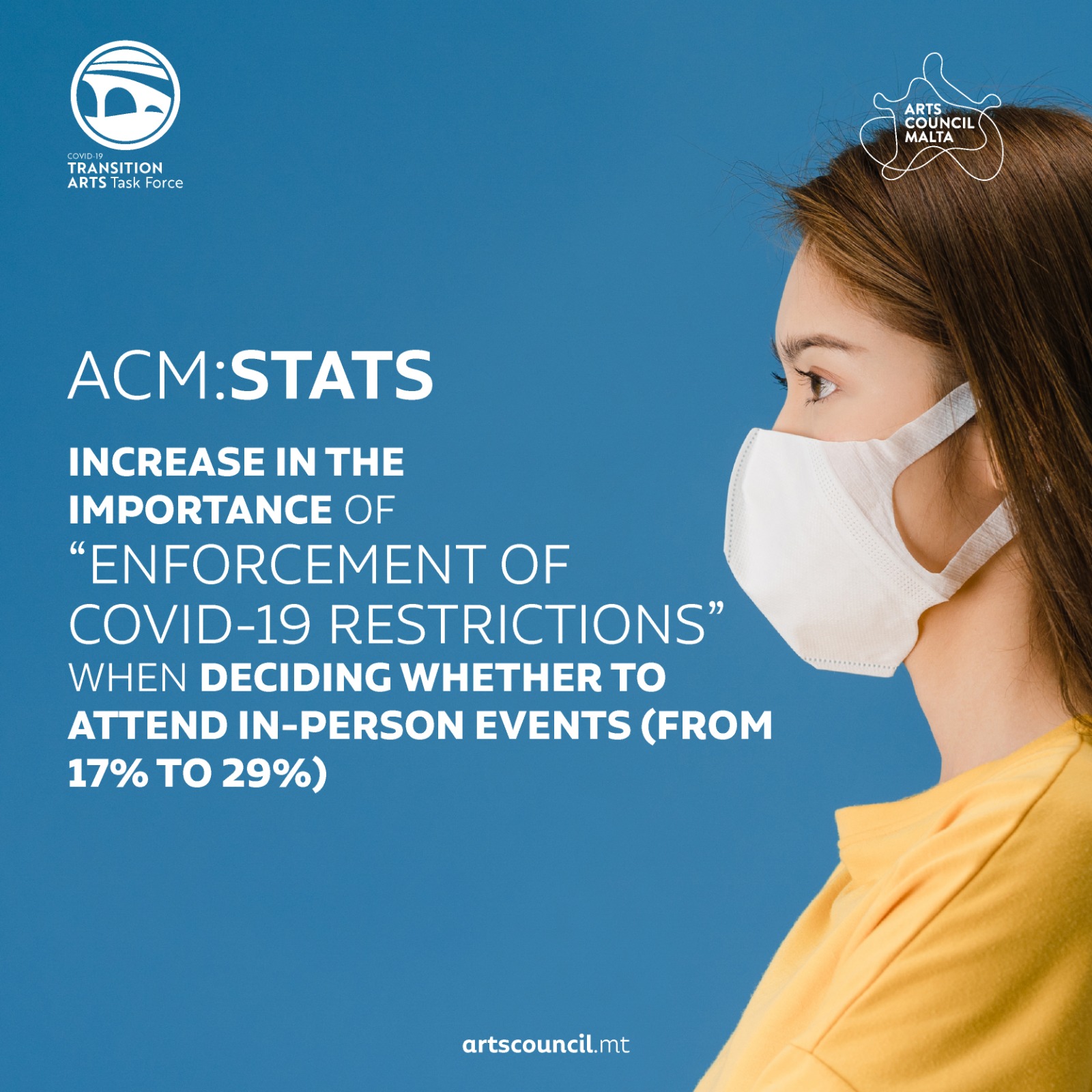

The study found that health-related concerns were still important factors when making a decision on whether to physically attend cultural events. Although the importance of having a vaccine decreased over time, from 32% to 20%, as more people were vaccinated, the importance of enforcing COVID-19 restrictions during events increased from 17% to 29% over the same period. The mention of “restricting audience sizes” as a factor to encourage attendance also increased from 8% to 12%, indicating a possible trend away from larger-scale events in favour of more intimate, smaller-scale activities.

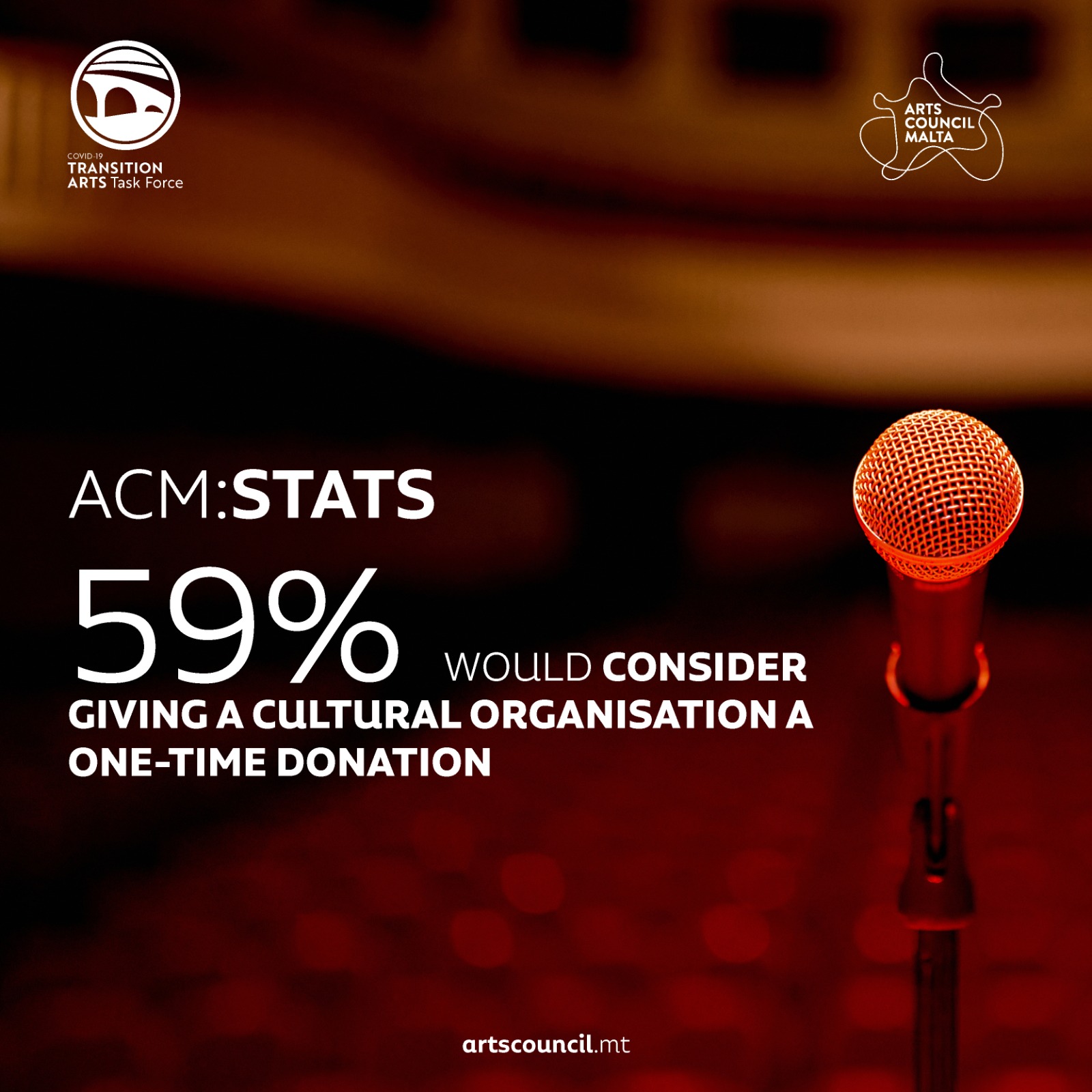

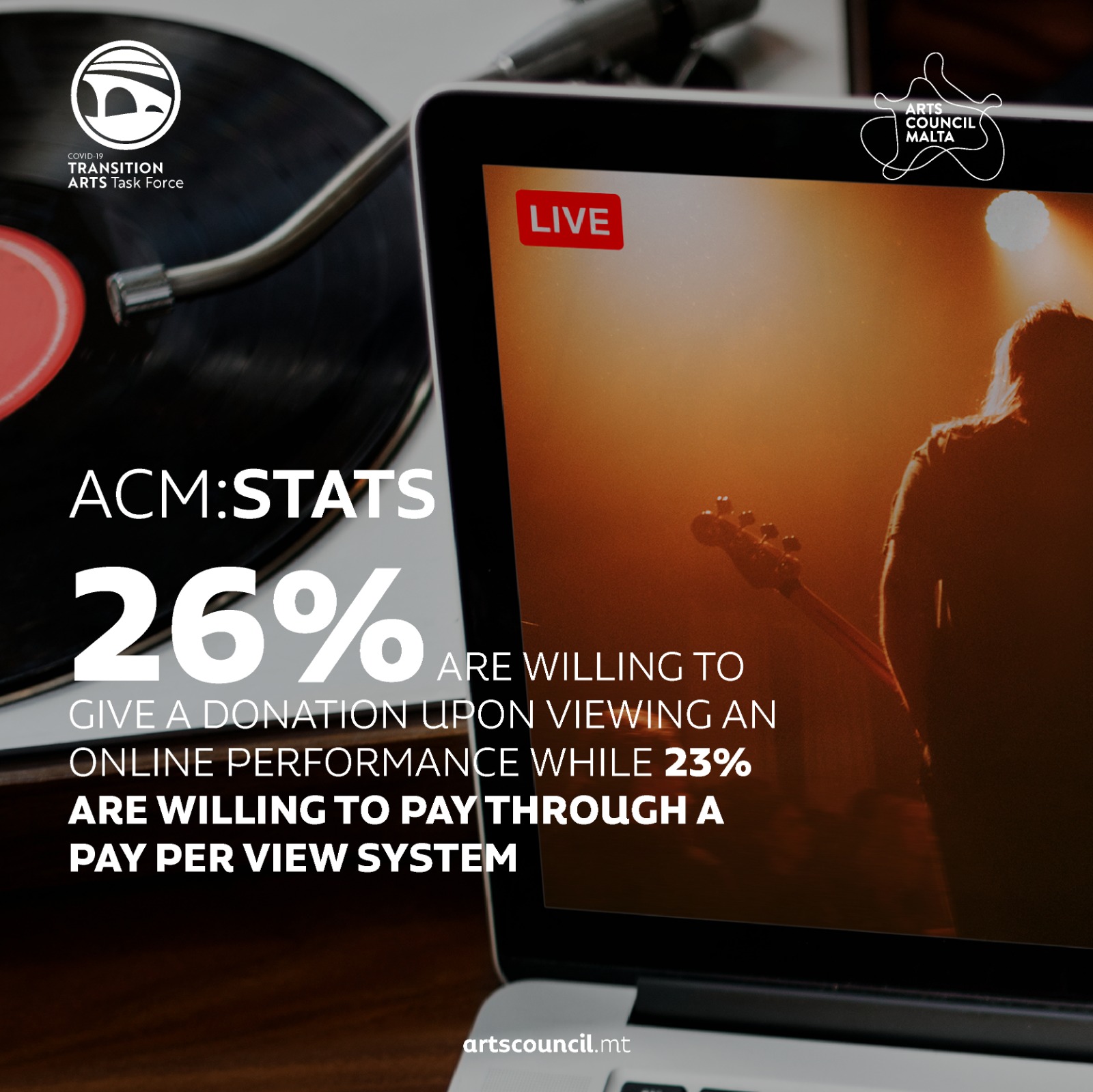

The study found that respondents seemed to appreciate the adverse effects that COVID-19 had on the cultural sector, and many are willing to financially support cultural organisations in some manner. 44% are willing to pay to attend events that were previously free, and 59% would consider giving a cultural organisation a one-time donation. A further 37% indicated that they are willing to pay a higher than average price (up to 10%) higher to attend a cultural event. Furthermore. 26% of respondents are willing to give a donation upon attending an online cultural performance, while 23% are willing to pay through a pay-per-view system.

Submitting ...

Saving ...

Any applications related to this entity, will also be automatically deleted.