The project budget template is an essential part of the application form and needs to be filled correctly in order for your application to be processed and evaluated. In the budget section you are required to fully outline both the income and expenditure, and also include any supporting documentation as required, if this is available at application stage.

The RESTART Schemes have a funding intensity that varies between 60% and 100%. The schemes support the amounts indicated as Co-Funding in the table below. The applicant is required to co-fund, or find other sources to co-fund the remaining percentage of the costs required to implement the project (for example 20% in the case of an 80% Co-Funding intensity).

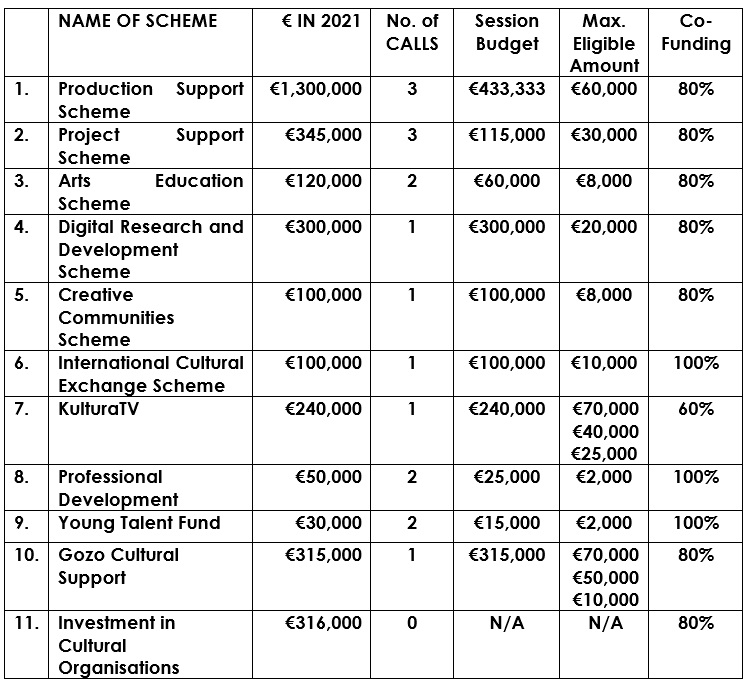

The table below provides an overview of the total amounts per scheme, the number of calls in 2021 and the session budget for each call. The maximum eligible amount is the maximum amount of each grant that the scheme may support. For more details, refer to the guidelines of the specific funding programmes.

These budget guidelines are for prospective applicants of the RESTART Schemes offered by Arts Council Malta. All schemes are competitive and it is advisable to read these guidelines before you submit your application.

Completing the budget section

The budget section in the online application gives the evaluators the necessary information needed to be able to consider the financial viability of your proposed activity. The budget template is an essential tool to outline the costs (expenditure) and forecast the amount of money it will generate (income) as well as any other funding already secured or needed to ensure the feasibility of your activity. It is crucial that you provide a realistic budget based on supporting documentation.

This guidance will help you to present a balanced budget, and we advise you to provide a clear breakdown for each entry to show us how you have reached your figures.

In this section of the budget, you need to provide details of the cash income for your application. You need to specify whether each income item has already been secured, is being negotiated or planned. A clear breakdown of all income is strongly suggested.

Types of income may include:

In this section of the budget, you are required to outline in detail all the expenses related to your application. The eligible costs vary from one scheme to another; refer to section three in the guidelines for more detailed information about what costs are supported by each scheme, and what costs are not supported by each scheme.

Types of expenditure may include:

In-kind contribution, as opposed to cash contribution, is used to describe any materials or services that are provided free of charge or at a reduced rate, and demonstrates a third-party backing or investment in the proposed activity that you are seeking funding for. The value of in-kind support contributes towards other funding required from other sources.

In-kind contribution should be included under both the “income” and “expense” with the same amount. In other words, in-kind contribution cannot be accumulated, and it has value only when and if it is used.

Examples of in-kind contribution include the following:

In-kind contributions do not include:

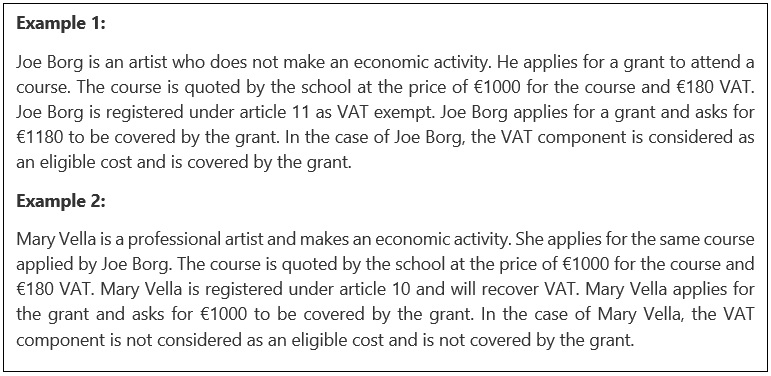

Any entity or individual who performs an economic activity must register for VAT. Kindly ensure that your VAT status is according to the regulations issued by the Commissioner for Revenue.

When filling the application you will be required to tick whether you are registered under article 10 or if you are registered under article 11.

Applicants registered under article 10 and who will recover VAT that is charged by third parties, any VAT amount will not be covered by the grant. Applicants who are registered under article 11 and are VAT exempt may include VAT charged to them by third parties as an eligible cost.

When submitting a quote to the council, this must always include VAT. The amount of the quote that is claimed through the grant, however, needs to be calculated according to the article under which the applicant is registered.

Should the application be funded, a contract between Arts Council Malta and the beneficiary will be signed. The contract will indicate the type of reports that the beneficiary will submit to the Council. Each report will include a budget form. VAT invoices and/or fiscal receipts need to be submitted together with the budget form.

It is important to ensure that a VAT invoice and/or a fiscal receipt is supporting each budget item. Amounts that are not supported by a VAT invoice or a fiscal receipt may not be covered by the grant.

Please refer to the Office of the Commissioner for Revenue website for more information related to VAT (https://cfr.gov.mt/en/vat/general_information/Pages/default.aspx). A list of frequently asked questions related to VAT is available on the following link: https://cfr.gov.mt/en/faqs/Pages/VAT/VAT-FAQs.aspx.

Ensure that all the financial aspects described in the narrative part of your application correspond and relate to the items listed in the budget and vice versa. The budget is another means to present your proposed activity and it should complement your application narrative.

Identify all possible sources of income in the budget, and make sure to indicate whether they are secured, unsecured or planned.

Double check your budget and make sure your request for funding falls within the funding limit of the funding programme.

Ensure that income projections are realistic and based on evidence and/or previous experience.

Provide all necessary supporting documentation.

If you need assistance when compiling the budget section of your application please contact our brokerage service team on 2334 7230 or email us on fundinfo@artscouncil.mt. Kindly note that we cannot read full applications before they are submitted.

Furthermore, Arts Council Malta provides a range of information sessions for its Funding Programmes as well as free-to-attend workshops to help you familiarise yourself with the funds. Contact us for more information.

Submitting ...

Saving ...

Any applications related to this entity, will also be automatically deleted.